Hailstorms in Texas do not play around. One strong storm can leave a roof bruised, shingles fractured, gutters dented, and water slowly working its way into places homeowners cannot even see yet. That is exactly why understanding the difference between a Public Adjuster vs. Insurance Adjuster for Hail Claims in Leander, TX matters so much before you file a claim or accept a settlement. Many homeowners assume all adjusters serve the same purpose.

They do not. In reality, public adjusters and insurance adjusters work from completely different perspectives. One represents the insurance company. The other represents the policyholder. That distinction changes everything during a hail claim, especially when the damage is extensive or the settlement offer feels incomplete.

And in Central Texas, incomplete hail claims happen more often than people think. I have seen situations where visible shingles were included in the estimate while damaged flashing, underlayment, vents, fencing, and soft metals were left out entirely. The homeowner thought the estimate was final. Then the contractor started repairs and discovered major gaps in the scope. That creates stress fast. This guide breaks down the real-world differences between public adjusters and insurance adjusters, how hail claims are evaluated, where disputes commonly happen, and when professional representation can genuinely change the outcome of a claim.

Why Hail Claims Become Complicated in Texas

Texas experiences some of the most aggressive hail activity in the country. Roof systems absorb repeated punishment from UV exposure, wind, heat expansion, and seasonal storms long before hail even enters the picture. Then the storm arrives.

Suddenly a roofing system that already carried years of environmental stress develops fractured shingles, loosened granules, lifted seams, punctures, and compromised waterproofing layers.

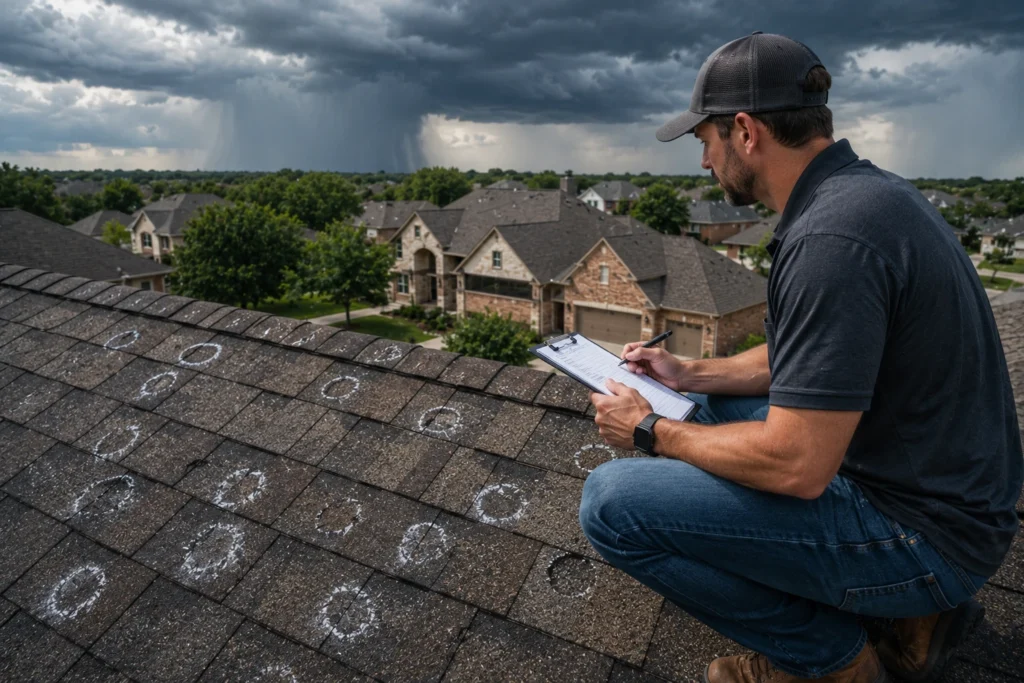

The challenge? Not all damage is obvious from the ground.

Some hail damage appears immediately. Other forms slowly reveal themselves over time through leaks, moisture intrusion, or accelerated roof aging. That delayed damage is where claim disagreements often begin.

Insurance carriers want to determine:

- What damage was directly caused by the storm

- What damage existed beforehand

- Whether repairs are sufficient

- Whether replacement is justified

- How much the carrier owes under the policy

At the same time, homeowners want enough funding to fully restore the property. Those goals do not always align perfectly.

What Is an Insurance Adjuster?

An insurance adjuster is the professional assigned by the carrier to inspect damage and evaluate the claim on behalf of the insurance company. That does not automatically make them dishonest or unfair. But it does mean they represent the insurer’s interests during the process.

Their role includes:

- Inspecting the property

- Reviewing policy coverage

- Documenting storm damage

- Preparing repair estimates

- Determining claim value

- Recommending payment amounts

Insurance adjusters generally fall into two categories.

Staff Adjusters

These adjusters work directly for the insurance company as employees. They handle claims internally and follow carrier-specific procedures and guidelines.

Independent Adjusters

Independent adjusters are third-party contractors hired by carriers, especially after major storms when claim volume explodes. After large hail events in Texas, carriers often deploy independent adjusters rapidly to keep up with demand. That means inspections may happen under tight scheduling pressure. Sometimes very tight. A single adjuster may inspect multiple roofs in one day during peak storm season. That workload can affect how detailed inspections become.

What Insurance Adjusters Typically Look For

Insurance adjusters focus on identifying covered storm-created damage under the terms of the policy. During a hail claim inspection, they often evaluate:

| Roofing Component | What They Assess |

| Shingles | Bruising, granule loss, fractures |

| Metal Components | Dents and impact marks |

| Flashing | Separation or punctures |

| Gutters | Functional hail impact |

| Siding | Visible storm damage |

| Interior Areas | Water intrusion evidence |

They also review whether the damage appears functional or cosmetic. That distinction matters a lot. Some carriers argue certain forms of hail damage are cosmetic only and do not affect roof performance. Homeowners and contractors often disagree strongly with those conclusions. This becomes one of the biggest dispute areas in hail claims.

Limitations Homeowners Should Understand

Many homeowners assume the insurance inspection automatically captures everything. That assumption can become expensive. Insurance adjusters work within carrier systems, time constraints, policy guidelines, and claim handling procedures. Even highly experienced adjusters can miss damage during busy storm seasons.

Common issues include:

- Limited roof access

- Short inspection windows

- Missed collateral damage

- Incomplete measurements

- Overlooked code requirements

- Underestimated labor costs

- Missing line items

Sometimes the initial estimate is accurate. Sometimes it is not even close. That is why homeowners should always review estimates carefully before repairs begin.

What Is a Public Adjuster?

A public adjuster works exclusively for the policyholder rather than the insurance company. That is the core difference. Their responsibility is to protect the homeowner’s financial interests during the claim process and pursue the full amount owed under the policy.

A public adjuster may assist with:

- Independent property inspections

- Damage documentation

- Policy analysis

- Estimate preparation

- Supplement negotiations

- Claim disputes

- Reinspections

- Settlement discussions

Unlike insurance adjusters, public adjusters are hired directly by the homeowner. Their compensation is typically a percentage of the final settlement amount. Because of that structure, public adjusters are motivated to identify overlooked damage, strengthen documentation, and negotiate for a more complete claim payout.

Public Adjuster vs. Insurance Adjuster for Hail Claims in Leander, TX

The biggest difference between the two comes down to representation. Here is a simple breakdown.

| Factor | Insurance Adjuster | Public Adjuster |

| Represents | Insurance company | Policyholder |

| Goal | Evaluate claim for carrier | Maximize covered recovery |

| Hired By | Insurance company | Homeowner |

| Payment Source | Carrier salary/contract | Percentage of settlement |

| Negotiation Position | Carrier-focused | Policyholder-focused |

This difference shapes the entire claim process. An insurance adjuster evaluates the claim through the carrier’s framework. A public adjuster evaluates the claim through the homeowner’s interests. That creates very different approaches during inspections and negotiations.

Inspection Differences Matter More Than People Realize

Insurance inspections after hailstorms can move fast. Very fast. Adjusters may inspect multiple properties daily after major storms. Their inspections often prioritize visible storm-created damage and standard carrier documentation procedures. Public adjusters usually approach inspections differently.

They often perform:

- Detailed photo documentation

- Full-scope evaluations

- Line-by-line estimate analysis

- Moisture detection reviews

- Code compliance checks

- Supplemental damage investigations

The level of detail can become especially important when roofing systems have layered damage from years of weather exposure. In many cases, the initial carrier estimate focuses only on immediately visible damage while deeper roofing components receive little attention until contractors begin repairs. That is where supplements enter the conversation.

Why Supplements Become So Important

A supplement is essentially an adjustment to the original insurance estimate after additional damage or costs are discovered. Supplements happen constantly in hail claims.

Why? Because roofing systems are complex.

Once contractors begin removing shingles, they may uncover:

- Damaged decking

- Compromised underlayment

- Improper ventilation

- Code upgrade requirements

- Additional flashing damage

- Ice and water barrier issues

- Hidden moisture intrusion

Those costs may not appear in the initial estimate. This is exactly why many homeowners begin researching Hail Damage Claim Supplements after contractors uncover additional roofing issues that were not included in the original insurance estimate. An experienced public adjuster often helps organize documentation supporting these additional items and negotiates them directly with the carrier. That process can significantly affect final settlement amounts.

Common Hail Claim Problems Homeowners Face

The reality is simple. Many hail claims become frustrating. Here are some of the most common problems homeowners encounter.

Low Initial Settlement Offers

Initial estimates sometimes fail to capture the full repair scope. This leaves homeowners struggling to complete proper repairs within budget.

Roof Repair vs Roof Replacement Disputes

Carriers may approve repairs for isolated sections while homeowners and contractors argue full replacement is necessary for matching or functional reasons.

Missed Components

Some estimates overlook:

- Ridge caps

- Gutters

- Window screens

- Flashing

- Siding

- Fence staining

- HVAC fins

- Downspouts

Those omissions add up quickly.

Delays

After major storms, claim volume surges dramatically. Reinspections, supplemental reviews, and administrative backlogs can extend the process for weeks or months.

How Public Adjusters Strengthen Claim Documentation

Strong documentation changes claim outcomes. Weak documentation weakens negotiating power. Public adjusters often focus heavily on evidence gathering because insurance carriers pay based on documented loss.

That documentation may include:

- Wide-angle roof photography

- Close-up hail impact photos

- Weather reports

- Date-of-loss verification

- Contractor reports

- Moisture readings

- Material testing

- Code citations

- Repair estimates

Some advanced roofing evaluations even resemble layered systems analysis found in fields like Topological data analysis, where patterns and hidden structural relationships become easier to identify through detailed inspection methods. The more organized and detailed the evidence becomes, the stronger the homeowner’s negotiating position typically is.

Understanding Xactimate and Why It Matters

Most large property claims use estimating software called Xactimate. This software helps generate standardized pricing for labor, materials, and repair procedures based on geographic region.

But software alone does not guarantee accuracy.

The estimate still depends on:

- Proper measurements

- Correct line items

- Accurate quantities

- Updated pricing

- Complete scope inclusion

Two adjusters can inspect the same roof and produce dramatically different estimates depending on how thoroughly the damage was documented. That is one reason why disputes happen so frequently in hail claims.

When Hiring a Public Adjuster Makes Sense

Not every claim requires public adjuster representation. Some smaller claims resolve smoothly. Others become complicated immediately.

A public adjuster may make sense when:

- The claim was denied

- The payout seems too low

- Major damage exists

- Multiple structures were affected

- Reinspections keep happening

- Policy language feels confusing

- Contractors identify major estimate gaps

- Commercial properties are involved

Large or disputed claims often benefit most from professional representation because the financial stakes become much higher.

Situations Where Insurance Estimates May Be Sufficient

It is important to stay balanced here. Some insurance adjusters produce fair, detailed, accurate estimates. Not every claim becomes adversarial.

A straightforward claim with limited damage may not require additional representation if:

- The scope appears complete

- Repairs are fully covered

- Contractors agree with pricing

- No disputes exist

- Settlement timing is reasonable

Homeowners should still review the estimate carefully, though. Even small omissions can create repair complications later.

Why Local Experience Matters in Hail Claims

Central Texas roofing systems face unique weather conditions. That matters during inspections.

Roofs in this region experience:

- Intense UV exposure

- Heat expansion stress

- High winds

- Sudden temperature swings

- Heavy seasonal storms

Those conditions accelerate material aging over time.When hail impacts already stressed roofing materials, the resulting damage patterns can become more complicated than homeowners expect.

Local experience helps adjusters understand:

- Regional storm behavior

- Common roofing systems

- Local labor pricing

- Municipal code requirements

- Area contractor practices

That regional understanding often becomes valuable during disputes involving roof replacement scope or repair feasibility.

The Emotional Side of Hail Claims

This part rarely gets discussed enough. Hail claims are stressful.

Families suddenly deal with:

- Leaking roofs

- Contractor visits

- Insurance paperwork

- Financial uncertainty

- Repair scheduling

- Interior damage concerns

People become overwhelmed fast. Completely understandable. That stress sometimes pushes homeowners to accept the first settlement simply to move forward quickly. But rushing the process can create long-term repair problems if the scope was incomplete from the beginning. Slowing down enough to fully evaluate the claim often protects homeowners financially later.

Red Flags Homeowners Should Watch For

Certain warning signs deserve closer attention during the claim process.

Repeated Reinspections Without Resolution

Multiple inspections with little progress may indicate ongoing disagreement about scope or coverage.

Extremely Fast Inspections

If an inspection feels rushed, homeowners should carefully review the resulting estimate.

Missing Roofing Components

Estimates should account for all affected systems, not just shingles.

Large Contractor Estimate Gaps

If reputable contractors consistently identify major differences from the carrier estimate, further review may be necessary. Coordination between adjusters and contractors often improves claim organization.

Mistakes Homeowners Should Avoid After a Hailstorm

Mistakes during the first few days after a storm can weaken the claim later. Avoid these common issues.

Waiting Too Long to Document Damage

Take photos immediately after the storm if it is safe.

Throwing Away Damaged Materials

Preserve evidence whenever possible.

Accepting Settlements Too Quickly

Review the estimate carefully before agreeing to repairs.

Hiring Storm Chasers

Verify contractor licensing, reputation, and local presence.

Ignoring Small Signs of Damage

Minor leaks often become major repair costs later.

Why Roof Matching Disputes Become So Frustrating

One of the most emotional parts of hail claims involves matching. A carrier may approve repairs for isolated roof sections while homeowners worry the repaired areas will not match the remaining roofing materials.

This issue becomes more difficult with:

- Older shingles

- Discontinued materials

- Sun-faded roofs

- Specialty roofing systems

The homeowner sees the property as a whole. The carrier may evaluate individual damaged sections separately. That disconnect creates tension during negotiations.

Commercial Hail Claims Add Another Layer of Complexity

Commercial claims often involve far larger financial exposure.

These properties may include:

- Flat roofing systems

- HVAC networks

- Drainage systems

- Skylights

- Mechanical penetrations

- Multiple structures

The documentation process becomes much more detailed. Public adjusters frequently assist commercial property owners because the scope analysis, code review, and negotiation demands become far more intensive than standard residential claims.

Timing Can Affect Claim Outcomes

The sooner damage is documented, the better. Why? Because weather exposure continues after the storm. Additional rain, heat, and wind can worsen existing damage or complicate the inspection process later.

Quick documentation helps establish:

- Storm timing

- Fresh impact evidence

- Initial property condition

- Damage progression

That evidence becomes especially important if disputes emerge later in the process.

The Financial Risk of Underpaid Claims

Underpaid claims do more than create temporary frustration. They can produce long-term property problems. Incomplete repairs may eventually lead to:

- Interior leaks

- Mold growth

- Structural deterioration

- Reduced home value

- Future insurance issues

And once repairs are completed improperly, recovering additional funds later becomes far more difficult. That is why careful estimate review matters so much during the early stages of a claim.

Public Adjuster vs. Insurance Adjuster for Hail Claims in Leander, TX: Which One Is Right for You?

The answer depends on claim complexity. Some homeowners only need the insurance inspection because the claim proceeds smoothly and the settlement fully covers repairs.

Others encounter:

- Denials

- Scope disputes

- Delays

- Incomplete estimates

- Repeated reinspections

- Large contractor discrepancies

Those situations often benefit from professional representation. The key is understanding your options early instead of waiting until frustration escalates.

Why Homeowners in Leander Should Take Hail Damage Seriously

Properties in Leander regularly experience severe weather exposure throughout the year. That ongoing environmental stress weakens roofing systems over time before hail even strikes. Once a major storm arrives, damage often spreads beyond what is visible from the ground. Many homeowners in Leander discover problems weeks later when leaks, moisture stains, or ventilation issues begin appearing after the initial inspection already occurred. That is why thorough evaluations matter so much.

Final Thoughts

Understanding the difference between a Public Adjuster vs. Insurance Adjuster for Hail Claims in Leander, TX can completely change how homeowners approach the claim process. Insurance adjusters serve an important role in evaluating claims for carriers. Public adjusters serve a different role entirely by advocating for policyholders during complex or disputed losses. Neither automatically guarantees a perfect outcome.

But knowledge matters. The more homeowners understand about inspections, documentation, supplements, roofing systems, and negotiation dynamics, the better positioned they become to protect their property and financial interests after a storm. Hail claims move fast. Decisions happen quickly. Stress builds even faster. Taking time to review the estimate carefully, document damage thoroughly, and understand who represents whom during the process can make an enormous difference when the repairs finally begin.

FAQs

An insurance adjuster works for the insurance company, while a public adjuster represents the policyholder during the claim process.

It depends on the complexity of the claim. Public adjusters are often helpful for denied, underpaid, or large hail claims.

Yes. Public adjusters commonly assist with Hail Damage Claim Supplements when additional damage is discovered after the initial estimate.

Yes. Fast inspections, heavy storm volume, and hidden roofing issues can sometimes lead to incomplete estimates.

Most public adjusters charge a percentage of the final insurance settlement amount.

Document the damage immediately, schedule a professional inspection, and review your insurance estimate carefully before repairs begin.

Yes. Homeowners can request reinspections, provide contractor documentation, or hire a public adjuster to help negotiate the claim.

Insurance companies may recommend repairs while contractors believe the roof requires full replacement due to functional or matching concerns.

Xactimate is estimating software commonly used to calculate labor, material, and repair pricing for property insurance claims.

Simple claims may resolve quickly, but disputed or supplemental claims can take several weeks or months depending on complexity.